Foreign Exchange Act and Crypto Restrictions in Bangladesh: Legal Gaps Explained

Imagine trying to buy a digital asset in a country where the law says you can’t hold it, yet the app store lets you download the trading platform without a hitch. That is the daily reality for many people interested in cryptocurrency in Bangladesh. The situation here isn't just about strict rules; it’s a messy mix of old laws, central bank warnings, and legal loopholes that leave everyone guessing what is actually enforceable.

If you are looking at the financial landscape in Dhaka or anywhere else in the country, you need to understand that while the government claims a total ban exists, the legal foundation for that ban is surprisingly shaky. This article breaks down exactly how the Foreign Exchange Regulations Act of 1947 (FERA) interacts with modern digital assets, why experts say the ban might not hold up in court, and what this means for your money.

The Core Conflict: Old Laws vs. New Tech

To understand why cryptocurrencies face such heavy restrictions, we have to look at the legislation governing foreign exchange. The primary tool used by authorities is the Foreign Exchange Regulations Act of 1947 (FERA). This law was written decades ago, long before Bitcoin existed, to control traditional currency flows in a post-independence economy. It defines "currency" very specifically under Section 2(b).

According to FERA, currency includes:

- Currency notes, postal orders, cheques, drafts, travelers' cheques, letters of credit, bills of exchange, and promissory notes.

- Any other instrument that the Bangladesh Bank declares as currency via an official notification in the Gazette.

Here is the catch. Bitcoin, Ethereum, and other tokens do not fit into the first category. They are not paper notes or checks. More importantly, the second category requires a specific legal action: the Bangladesh Bank must officially declare these digital assets as "currency" through a statutory notification. As of now, no such notification has been issued. This creates a massive legal gap. Without that declaration, arguing that holding Bitcoin violates FERA is legally questionable because the statute simply doesn't define it as prohibited foreign exchange.

Bangladesh Bank’s Stance and Practical Bans

Despite the legal ambiguity in the text of the law, the Bangladesh Bank, which serves as the central banking authority, has taken a hardline approach. Since 2017, the central bank has issued multiple circulars warning citizens against using, trading, or possessing cryptocurrencies. Their stated reasons include preventing money laundering, stopping terrorism financing, and protecting the stability of the national financial system.

In practice, this prohibition works through pressure on commercial banks rather than direct police raids on individuals. Banks are instructed to block transactions linked to known cryptocurrency exchanges. If you try to send Taka to a wallet address or an exchange like Binance using your local bank account, the transaction will likely be flagged and reversed. The central bank views any attempt to move funds out of the formal banking system into unregulated digital markets as a threat to monetary control.

This practical ban extends beyond just trading. Possession itself is discouraged, though enforcement varies. The goal is to keep all financial activity within the supervised banking sector, where the government can monitor flows and enforce anti-money laundering (AML) standards.

The Underground Market and How People Trade Anyway

Laws on paper often differ from reality on the ground. In Bangladesh, a thriving underground market for digital assets continues to operate despite the official prohibitions. You can still find major applications like Binance and KuCoin listed on the Google Play Store. While some features may be restricted or accounts frozen if linked to local bank cards, the technology remains accessible.

So, how do people actually buy crypto? They use informal networks. Local agents act as intermediaries, facilitating peer-to-peer (P2P) trades. An individual wants to buy Bitcoin; they transfer Bangladeshi Taka to a local agent’s bank account or mobile wallet. The agent then transfers the equivalent value in cryptocurrency to the buyer’s digital wallet. These agents charge a small commission for taking on the risk. This method bypasses the direct link between the user and the international exchange, making it harder for banks to flag the initial Taka transfer as crypto-related.

However, this comes with significant risks. There is no consumer protection. If an agent disappears with your money, or if the government cracks down on these networks, users have little recourse. The National Board of Revenue (NBR) also monitors large cash movements, so relying on informal channels carries both legal and security dangers.

Taxation: A Paradoxical Framework

One of the most confusing aspects of the current regime is taxation. The National Board of Revenue (NBR), which handles tax collection, operates under the Income Tax Ordinance of 1984. Currently, there is no specific law defining how to tax cryptocurrency profits. However, the general rule treats cryptocurrencies as property.

This creates a strange paradox. The central bank says you cannot trade crypto, but the tax authority implies that if you do make a profit from selling it, that gain is taxable income. Gains from the sale of digital assets could be subject to capital gains tax under general provisions. This lack of specific legislation leaves a regulatory gray area. Traders are unsure whether they should report their income, fearing that doing so admits to participating in an illegal activity, while ignoring it risks penalties for tax evasion later.

Experts suggest that the government is considering updates to provide clearer guidelines, but nothing concrete has been passed as of 2025. Until then, taxpayers are left navigating a system where the act of earning is technically banned, but the profit is theoretically taxable.

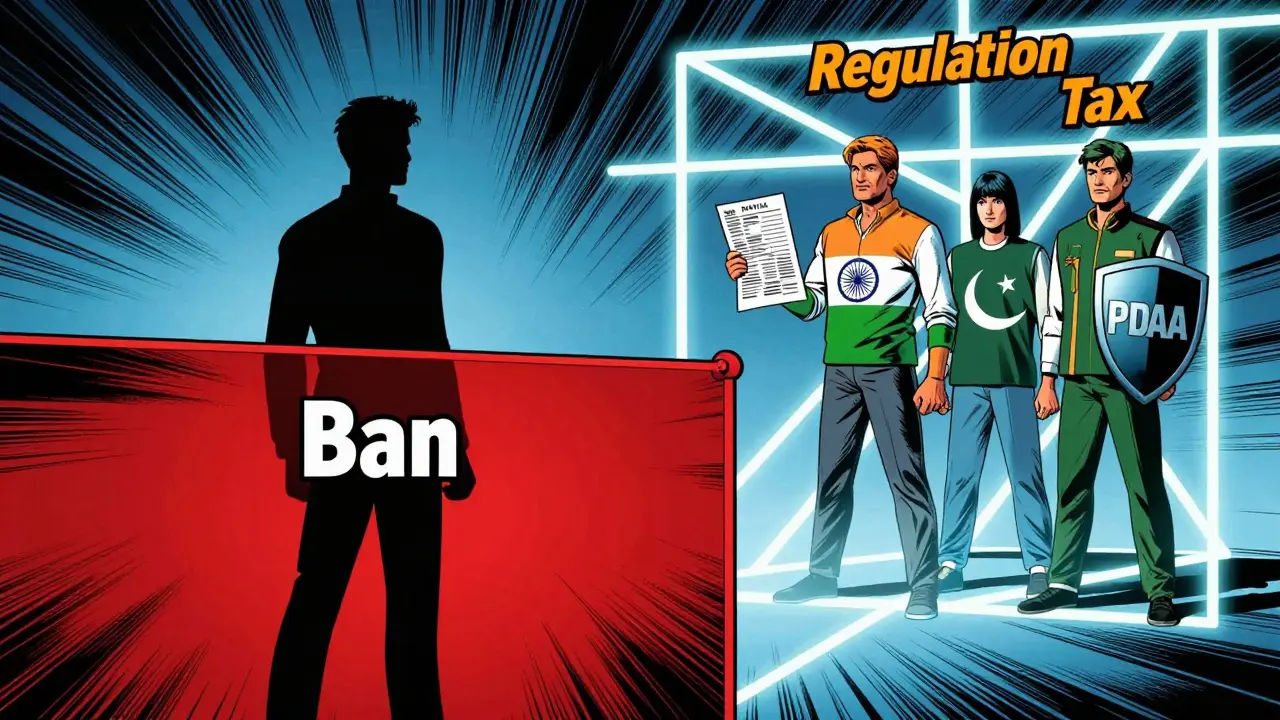

Regional Comparison: Isolation vs. Regulation

When you look at neighboring countries, Bangladesh’s isolation becomes stark. Other South Asian nations are moving toward structured regulation rather than outright bans. For instance, Pakistan established the Pakistan Digital Assets Authority (PDAA) in May 2025 to oversee exchanges and wallets. India implemented a clear tax framework with a 30% tax on crypto profits and a 1% Tax Deducted at Source (TDS), generating billions in revenue.

| Country | Regulatory Approach | Key Authority | Tax Status |

|---|---|---|---|

| Bangladesh | Strict Prohibition | Bangladesh Bank / FERA | Unclear / General Property Rules |

| Pakistan | Regulated Framework | Pakistan Digital Assets Authority (PDAA) | Defined Regulatory Oversight |

| India | Taxed & Regulated | Income Tax Department | 30% Profit Tax + 1% TDS |

This contrast highlights a potential economic cost for Bangladesh. By maintaining a comprehensive ban, the country misses out on the innovation, investment, and tax revenues seen in neighbors. It also pushes activity further underground, reducing transparency rather than increasing it.

Legal Expert Opinion and Future Outlook

Academic and legal experts in Bangladesh are increasingly vocal about the ineffectiveness of the current ban. Dr. B M Mainul Hossain, a professor at Dhaka University, has publicly argued that prohibition is not a sustainable solution. The sentiment among many professionals is that regulation would better serve public interests by bringing transactions into the light.

The persistence of the underground market proves that demand exists regardless of policy. The real question facing policymakers is whether to strengthen the legal basis for the ban by amending FERA to explicitly include digital assets, or to pivot toward a regulatory model similar to India or Pakistan. Given the definitional gaps in the 1947 Act, legal challenges to prosecutions under FERA could succeed, forcing the government to either update its laws or abandon the ban.

For now, the status quo remains: high risk, low clarity, and a reliance on informal networks. Anyone engaging with digital assets in Bangladesh does so at their own peril, navigating a system where the law lags far behind the technology.

Is cryptocurrency illegal in Bangladesh?

Technically, yes. The Bangladesh Bank prohibits the usage, trading, and possession of cryptocurrencies based on interpretations of the Foreign Exchange Regulations Act of 1947. However, legal experts argue that since cryptocurrencies are not explicitly defined as "currency" in the Act, the ban may not be fully enforceable in court.

Can I use Binance in Bangladesh?

You can download the app, but using it with local bank accounts is risky. Banks are instructed to block transactions linked to crypto exchanges. Many users rely on peer-to-peer (P2P) methods with local agents to avoid direct bank links, but this carries significant fraud and legal risks.

Do I have to pay taxes on crypto profits in Bangladesh?

There is no specific crypto tax law, but the National Board of Revenue treats cryptocurrencies as property. Profits from sales may be subject to capital gains tax under the Income Tax Ordinance of 1984. Reporting these profits is complicated by the fact that the underlying activity is technically prohibited.

Why does Bangladesh ban cryptocurrency?

The Bangladesh Bank cites concerns over money laundering, terrorism financing, and financial instability. They fear that unregulated digital assets could undermine the national currency and allow capital flight outside the controlled banking system.

How does Bangladesh's crypto policy compare to India or Pakistan?

Bangladesh maintains a strict prohibition, whereas India has implemented a structured tax regime (30% tax on profits) and Pakistan has established a dedicated regulatory authority (PDAA). Bangladesh is currently isolated in its restrictive approach compared to its regional neighbors.

The epistemological framework of the Foreign Exchange Regulations Act is fundamentally incompatible with the ontological reality of decentralized ledgers, yet the bureaucratic apparatus persists in its dogmatic adherence to archaic statutory interpretations. This creates a dialectical tension where the state’s coercive power is theoretically absolute but practically nullified by the very legal ambiguities it seeks to exploit. The notion that a 1947 statute can effectively govern 21st-century cryptographic assets is not merely outdated; it is an affront to logical consistency and economic rationality. One must question whether the central bank’s warnings are genuine attempts at financial stability or mere performative displays of authority designed to mask regulatory incompetence. The lack of explicit statutory notification declaring Bitcoin as 'currency' under Section 2(b) renders the entire prohibition legally voidable, exposing the government to significant liability should any citizen choose to challenge this in court. It is absurd that citizens are forced into underground economies because their leaders refuse to update legislation that predates the internet by decades.

I find myself deeply concerned about the implications of this regulatory vacuum for everyday citizens who are simply trying to navigate their financial futures in a rapidly evolving digital landscape, especially when we consider how neighboring countries like India and Pakistan have managed to create more structured environments that actually protect consumers rather than driving them into the shadows where fraudsters thrive without any oversight whatsoever. It is truly disheartening to see such a disconnect between policy and reality, as the people suffer the most from these indecisive measures while the authorities remain entrenched in their outdated methods of control that fail to address the actual needs of the modern economy.

It really sucks that people have to risk so much just to trade something that's basically becoming normal everywhere else. I feel bad for those using P2P agents because one wrong move and they lose everything, and there's no help coming from the banks or the government. It's a tough spot to be in.

i mean its kinda crazy how they say its illegal but then try to tax it? thats just messed up lol. nobody knows what to do and its scary.

Listen up! The ban is stupid and weak! Everyone knows you can get around it! Stop pretending you're protecting us when you're just blocking innovation! We need real rules now!

hey guys, i was wondering if anyone has tried using the p2p method safely? seems risky but maybe there are some good agents out there? just curious cuz the options are limited here.

This is pathetic. Absolute garbage. You people are blind to the obvious truth that this ban is just a cover for corruption and incompetence. While India makes billions, Bangladesh chokes on its own stupidity. The moral decay of ignoring clear global trends is nauseating. Wake up!

Oh my goodness, this is so stressful! How can anyone live like this? It feels like everyone is fighting against each other instead of working together. We really need peace and clarity, don't we?

You need to understand that the legal gap isn't just a technicality; it's a fundamental failure of governance! If you're holding crypto, you're technically safe until they fix the law, but don't let that lull you into a false sense of security! The banks will still freeze your accounts! Fight for regulation!

🚀 The irony is palpable! 🎭 They ban it, yet the app store stays open! 📱 It’s like playing hide and seek with your money! 💸 Smart folks use P2P, but watch out for scams! 👀 Let’s educate ourselves! 📚

The philosophical implication of banning technology while taxing its profits suggests a society that fears progress more than it values order. Silence speaks volumes here.

I believe that despite all these challenges and confusing laws and the fear of losing money or getting in trouble with the authorities, there is still hope for a better future where regulations make sense and everyone can participate fairly in the digital economy without having to hide in the shadows or worry about their funds being frozen arbitrarily by institutions that don't understand what they are regulating.

Just chill, man. It's what it is. People trade anyway. Don't overthink it.

The author clearly misunderstands the severity of FERA violations. While the definition of currency is narrow, the intent of the act is broad enough to encompass any instrument used for foreign exchange transactions, which crypto undoubtedly is. Ignoring this nuance is dangerous advice.

I think it's important to look at the facts without panic. The law is vague, yes, but the risks are real. Maybe we should focus on how to advocate for clearer rules rather than just criticizing the current system?

How quaint. A nation clinging to 1947 laws while the rest of the world moves forward. It’s almost adorable how they pretend this ban means anything. Truly, the height of bureaucratic delusion.

STOP HIDING! TRADE NOW! NO RULES! FREEDOM!